SAIP FinTech holdings Pt. 2💸

SAIP FinTech holdings Pt. 2💸

How to participate in the Financial Revolution

As we discussed in our last issue, the financial world is changing around us. There’s a revolution in Financial Technology (FinTech), which is remaking money and commerce as we know it. In this issue, we continue the discussion, diving further into Fintech, what it is, and how we can invest.

The traditional finance industry is being disrupted on multiple fronts. Payments are handled more efficiently by mobile-enabled platforms, lending and borrowing facilitated directly peer-to-peer, and digital currencies are increasingly supported by central banks. We are moving to a more decentralized financial model, and these are the companies and assets we have our eye on as it happens. 👀

Payments 💳

For generations, it’s been hard to imagine a world without banks. Visit any modern city, the tallest buildings usually have the biggest bank logos. From Midtown Manhattan and City of London to Hong Kong and Singapore, banking has a dominant and highly visible role globally.

Traditionally, banks have facilitated all interactions between people and money. They are there for everything — from buying groceries, to student loans, first houses, and booking holidays — banks are always holding the purse strings. Having institutions facilitating our financial life ensures that every money move is verified and secure. But it also means that these institutions are able to take hefty fees and act as middlemen in most transactions.

But these fees and legacy IT systems are weighing banks down in comparison to the fast, seamless, and user-friendly technology and devices that we interact with on a daily basis (you, me, and the 3.8 billion other smartphone users in the world). While banks struggle to keep up, consumers’ short attention spans are turning to their daily digital services to handle payments and transactions for them. In China, Ant Financial’s AliPay dominates with 1.3 billion users while in North America and Europe, Apple Pay and Google Pay help consumers make digital payments via mobile devices.

The common thread is that these services are provided by tech firms rather than banks. While banks have been with us through big moments in our lives, these services are with us every waking minute of every day. Our close relationship has allowed these firms to take the natural next step of offering us payment and financial services, in many cases replacing banks.

Fintech companies that have been able to build on the power of consumer technologies are thriving and taking market share from traditional banking. The proliferation of e-commerce has created opportunities for shopping and payments to be handled by the same services, breaking from the deeply rooted, traditional business models.

Investing in Fintech 💸

For investors, a great place to start is by looking at fast-growing payment and e-commerce companies that have excelled at maintaining a close customer relationship. Companies like Square Inc, PayPal Inc, Shopify, and MercadoLibre all have very impressive growth rates and are changing the way business is done online.

Ark Fintech Innovation ETF (NYSE: ARKF)

We always have an eye on how Cathie Wood and her team at Ark Invest are allocating their Fintech Innovation exchange-traded fund (ETF). We think you should too. This is a collection of top international Fintech stocks managed by a skilled investment team. We could do a whole article on Cathie Wood and her investing wisdom (and we probably will!). Ark Invest creates high-quality research and analysis on this subject, a key source of insight for SAIP, which is worth checking out.

Mercado Libre (NASDAQ: MELI)

At SAIP we own Mercado Libre, which is the largest e-commerce firm operating in Latin America. The company is comparable to Amazon with elements of Shopify and Square mixed in. They operate an e-commerce website, payment service, and logistics network. MercadoLibre is growing rapidly in a region where the overall use of e-commerce is much lower than in Europe and North America. In addition, they have an insane 69% growth rate in free cash flows, and revenue from their e-commerce business expanded by 90% in 2020.

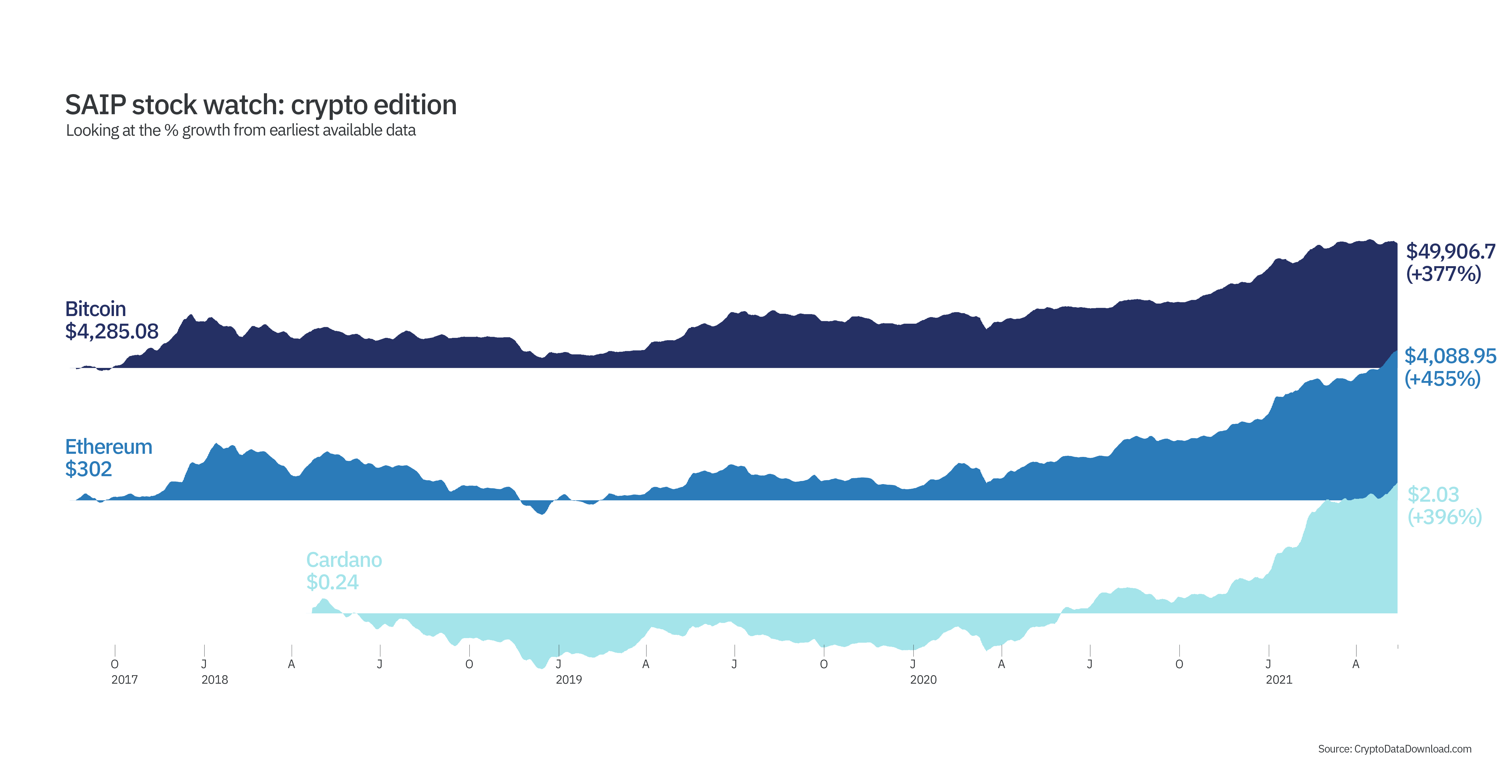

Crypto Asset Networks

At SAIP we hold several of the large cryptocurrencies as a store of value and as a hedge against weakening fiat currencies. Our core position here is Bitcoin, which is the largest and most mature cryptocurrency and digital asset. In addition, we are interested in the ‘decentralized finance’ or DeFi platforms that are growing rapidly following the success of Ethereum.

Bitcoin

The main cryptocurrency holding at SAIP is Bitcoin. Founded in 2009 by the mysterious and still-unidentified Satoshi Nakamoto. Despite what you might see in the media, there are no physical Bitcoins (they just need cool pics to keep people interested). The currency exists only on a digital ledger distributed among a network of computers called the ‘blockchain’.

The introduction of Bitcoin was revolutionary due to the way in which transactions can be made and verified without a third party in the middle. The underlying blockchain technology has since become a widely discussed architecture in its own right. In each ‘block’ is a set of transactions that have been verified by ‘miners’ running high-performance computing hardware and competing for newly minted Bitcoins. Once the miners have completed a block, it is added to the public Bitcoin blockchain which is stored on all computers or ‘nodes’ in the network.

We have included Bitcoin as a holding due to its security — the massive computing or ‘hashing’ power of the network. For someone to successfully attack the Bitcoin network, they would need to control 51% of the computing power, which is spread around the globe. In addition, it is the oldest cryptocurrency and therefore has the most substantial track record.

The complete decentralization of the network is also attractive along with the fact supply is capped at just under 21 million coins. No more than this can ever be minted, and scarcity is one of the most important qualities in monetary value.

But isn't Bitcoin mining carbon-intensive? Great question, and one we get a lot. We’ve thrown a lot of information at you already, so we’ll save our answer for an upcoming issue, where we’ll investigate the technology, data, and emissions behind bitcoin mining.

Ethereum

If Bitcoin is Batman of the cryptocurrency universe, then Ethereum is Robin. Launched in 2015, the founders of Ethereum aimed to create a more programmable and scalable blockchain-based architecture.

The platform allows developers to create ‘smart contracts’ which allow an agreement between buyer and seller to be written directly into code and stored across a distributed blockchain. This idea built upon Bitcoin’s innovations and allowed for increasingly trustless commercial relationships to be built without the usual legal systems and third parties which normally facilitate such transactions. Many large companies are building open-source projects on the Ethereum blockchain, including Microsoft and JP Morgan.

At SAIP, we’re interested in the developments in the Ethereum ecosystem and think that there’ll be substantial financial innovation coming from this community. We are holders of Ether (ETH), the cryptocurrency native to the Ethereum network.

Cardano

Cardano is among the largest cryptocurrencies by market cap and is a competitor to the Ethereum network, but using a newer ‘third-generation’ blockchain architecture. The network was founded by one of the co-founders of Ethereum. This network is aiming to enhance many of the features present in the Ethereum network including smart contracts via a more efficient network design, and collaboration across a group of academics around the world to ensure that updates are scalable.

—

If you didn’t believe us at first, hopefully after this discussion — and all the new words— you’ll agree our financial world is changing. Banks are being disrupted by scrappy start-ups and established tech giants, along with the governments and central banks looking to enter the digital currency race.

We are moving toward a new financial model whether we like it or not. To take advantage of the revolution, it’s important to understand the market dynamics pushing consumers toward the new services, and the properties that make digital assets and currencies likely to be adopted at scale. At SAIP, we’ll continue to keep you informed and up to date on how we’re navigating these new waters, so you too can ride the wave that is the FinTech Revolution. 💸

In the works📝

We’ve touched on what we have our eyes on in the crypto asset space. We plan to go into more detail in an upcoming issue about the crypto market and unpack the concept of ‘decentralized finance’ and how we are thinking about investing in this space. We will compare the decentralized with the centralized by discussing Central Bank Digital Currencies and why they will be important.

As promised, we’re also working on an issue, bringing together the two areas fundamental to SAIP: the Energy Transition⚡️ and Fintech Revolution 💸. With the recent announcement from Tesla and Elon Musk that they would stop accepting Bitcoin due to its climate impacts, we thought it would be a good time to investigate this issue and look at some of the data. We’ll explore the energy consumption and climate impact of Bitcoin, and how concerning it really is.

The data 📈

For this newsletter, we used two different datasets for two different charts. For the first SAIP stock watch, we used Google Finance data for each stock for the last 12 months. For SAIP stock watch: crypto edition, we used data from CryptoDataDownload.com. For both graphs, we visualized the data by using a one-week moving average of the total daily percent change for each holding. The percent change of the stock price is based on the one-week moving average not the % change of the stock price from the first date to the last date shown.

At SAIP, we're happy to help but you should not be blindly reading this and then sinking your life savings into these stocks. 😀 As with all investment decisions, each individual should undertake their own research and ensure that they are in a good financial position before investing in the stock market.

As always, we would love to hear from you and your thoughts on this month’s newsletter. We’re also interested to hear what topics you’d like us to explore for future issues. Please reply to this email or comment on the post with any topic recommendations, thoughts, or questions (or rebuttals — we love a good debate!).