Inflation: starting from the top to understand the impact today

Inflation has been making headlines lately and it's not good news. You only have to look to your inbox for evidence.

Our mobile phone bill went up by almost 9% since last year. Our internet has gone up 10% and our energy bill has almost doubled.

Inflation is a term we’ve all heard before. But most of us don't understand how complex and personal this monetary phenomenon really is. So what does inflation mean? What causes it? And why should you care?

Since we’re living through the highest inflation in the last half-century, we thought you’d like to know.

Time to rewind

The exchange of value is part of what makes us human. In the early days, exchanges were based on bartering. First, people on both sides had to agree on what was valuable.

Value was synonymous with scarcity. But there were other attributes too. To successfully be used as ‘money’, you had to be able to carry it, divide it, and it had to be durable.

1000s of years later

Gold and silver become the main medium of exchange. But in large amounts, it was hard to move and there was a security risk of having a lot of it.

Goldsmiths with vaults became the home base for gold. They’d give you a paper receipt with the amount and quality in return for gold deposited.

Paper was easy to carry and divide. Backed by the promise from a trusted institution, it was durable and secure.

Banking is born

Goldsmiths gave way to banking as we know it today. By holding society's gold, banks gave out loans and earned a profit.

Central banks or national banks, like the Bank of England, were created. In exchange for financing the nation’s government or monarchy, these new institutions would get sole rights to issue currency, or official ‘IOUs’.

For a long time, currency in circulation was directly exchangeable for gold. Having money backed by a scarce commodity like gold was called ‘hard money’, ensuring value and stability of the currency over time.

A broken bond

Since 1931 in the UK – and as recently as 1971 in the US – the connection between money and gold has been broken. Money is no longer directly redeemable with gold.

This new monetary system, where currencies are not backed by a scarce commodity, is commonly called ‘Fiat currency’. Removing gold from the equation freed central banks to increase the supply of Fiat currency as they saw fit.

How’d you like to pay?

Even without hoarding society’s gold, central banks still exist to finance governments. Governments generally have three options when it comes to balancing budgets:

Raising taxes

Cutting spending

Creating new money

The third option is the most tempting. Money is almost free to make and it solves a lot of problems. It also doesn’t rock the public boat like the first two options.

In 2008, the financial crisis shook the system. By creating new money and lending it to the government, central banks can stabilize the financial system in the short term, so that’s what they did.

Since then, when faced with big problems – like the COVID-19 pandemic – central banks have pressed print with a heavy hand.

To be fair, governments didn’t have a lot of choice during the pandemic. People weren’t able to work and the economic shortfall had to be made up somewhere. The bleak alternative would be depression and economic collapse.

But this short-term gain is set to cause significant global long-term pain.

Ok - but what is ‘inflation’?

As influential economist Milton Friedman said:

“Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

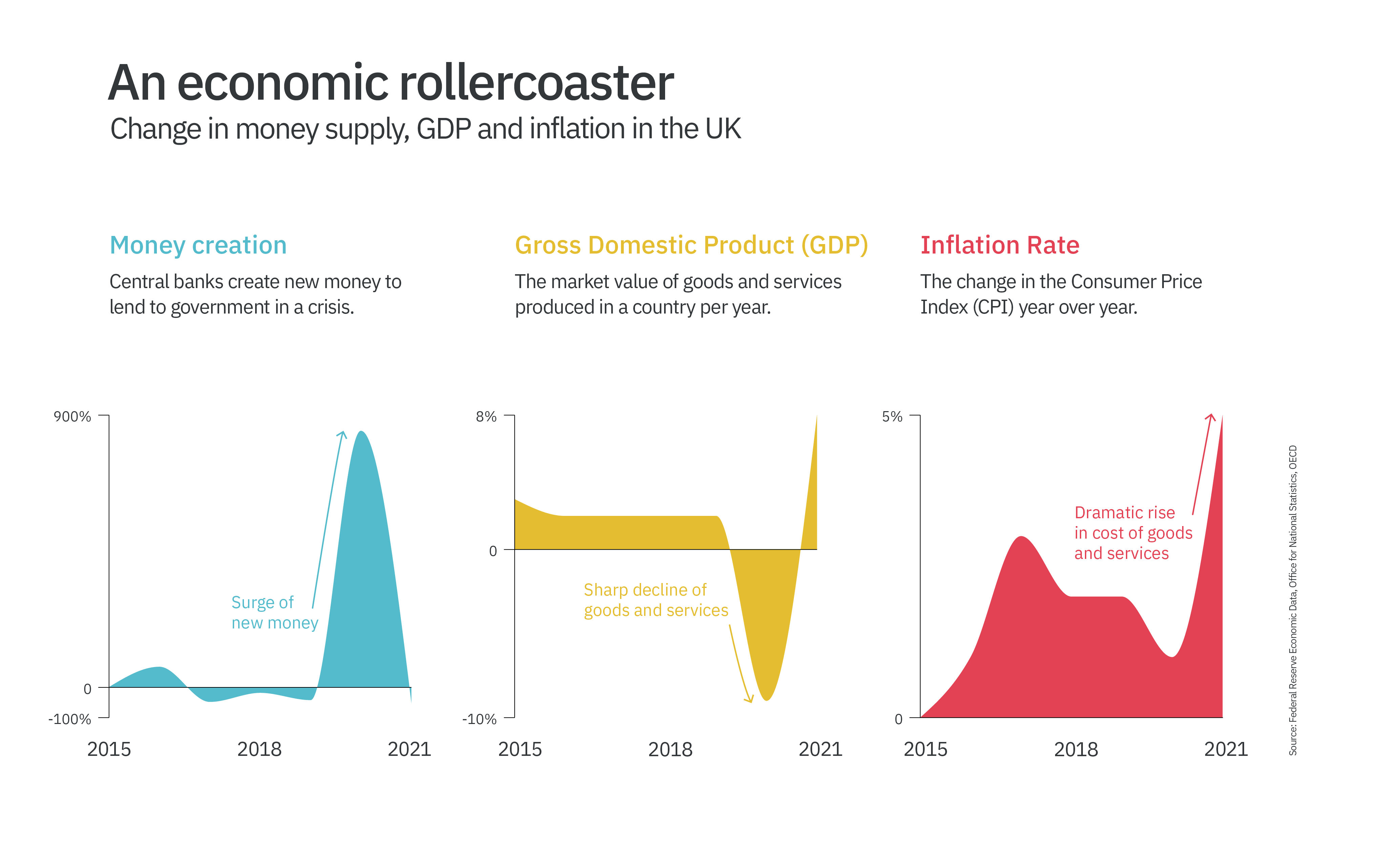

In other words, if a country’s supply of money grows faster than its output (GDP), that’s when inflation hits.

Prices stay consistent when the money supply grows alongside GDP but that’s not the current trend.

There’s more money being created but countries aren’t generating more goods and services. This means there’s more money to purchase the same amount of goods and services.

This causes each unit of currency to be worth less. To understand this shift let’s look at a real-life – but extreme – example.

Venezuela’s costly caffeine fix

Once the richest country in Latin America, Venezuela experienced a drastic case of inflation – or hyperinflation – starting in 2016.

Completely dependent on oil revenues, plummeting prices shocked the country. The government printed huge quantities of money to make up for obliterated budgets.

There was an influx of money but there were no extra goods and services to buy. More money in circulation and declining GDP caused prices to skyrocket, resulting in a 43,378% inflation rate.

You didn’t have to look further than a cup of coffee to see the effect – a coffee cost one million bolivars in 2018.

Venezuelan coffee didn’t get more valuable. Venezuelans just had to pay more for the same old cup of coffee because each bolivar became essentially worthless.

In 2018, one million bolivar equaled $0.29 USD. Banknotes were worth no more than the paper they were printed on.

We established that monetary value was synonymous with scarcity. In Venezuela, banknotes aren’t scarce, so they have next to no value.

This has caused some local communities to step back in time, resorting to bartering for food or creating their own local necessity-backed currencies.

Venezuelans are rewinding 1000s of years because their currency has failed them. Money devaluation has created complete economic and social collapse.

The case in Venezuela is extreme. But over the last two years in many countries, money creation outpaced GDP, causing the Consumer Price Index (CPI) - the price of a basket of everyday items – to rise quickly.

This is a big reason why we’re facing inflation at a higher rate than the western world has experienced in decades.

People pay the price

Citizens don’t respond well to a tax increase or budget cuts. But governments can create money out of thin air at citizens’ expense and without them really knowing.

Inflation is an under-the-radar way of taxing people in a country. That’s why it’s often referred to as ‘taxation without legislation’.

We all pay for money printing through inflation, now and into the future. CPI is rising and our cost of living is going up with it. But what does it mean for salaries and savings?

If you make £40,000 a year now, in twelve months, the same salary will be worth £37,800 (in terms of the value of goods and services you can purchase with it). In five years, it could buy just over £30,000.

If your savings are sitting still, the same principles apply. If you have £10,000 saved, in five years that same amount at the same inflation rate will be worth around £7,500.

Can this erosion be avoided?

There’s a lot of newly created money floating around looking for a home. People and companies with disposable income are putting it into assets, like the stock market, or real estate.

That’s why when the pandemic hit, the stock market didn’t suffer as much as everyone thought it would. And why the real estate market hit record highs.

There are not enough houses being built, so people have to bid up the price in order to secure a place to live.

Like most global catastrophes, inflation hits people with lower income harder. As expenses like rent increase, low-income households have less money to spend on necessities like food, medicine, and transportation.

Lower-income households generally have no investments and don't own their own home. So they haven’t benefited from the rise in the stock market or real estate prices.

But billionaires have. As cash was funnelled into the stock market, billionaire wealth shot up. For example, Elon Musk’s net worth – although mostly held in publicly-traded stock – jumped over 600% over two years.

All of this has increased inequality, making our political systems less stable.

—

An almost 80-year-old global system is unraveling. It has a direct effect on our life now and in the future – it’s personal.

It’s important to understand what’s pulling the strings behind rising prices. We’ve only scratched the surface of explaining this monetary phenomenon – there’s a lot more to dig into.

In the coming months, we’ll help you do just that. We’ll write about how you can fight against inflation and protect your savings.

In the mean time, one thing you can do is keep learning about the financial systems that support our day-to-day existence. Here are some resources we have been learning from:

Principles for Dealing with a Changing World Order by Ray Dalio (Book & YouTube video)

The School of Life - Inflation

Really clarifying newsletter in plain language. The Venezuela example, while extreme, reveals the essentials so clearly. Thank you SO much. I have recently started 'The Changing World Order' by Ray Dalio - highly readable, contemporary, timely and content rich. Looking forward to more. Keep em coming.

This blog is a valuable resource for readers.